On October 12th ISDA hosted a webinar together with the LSTA, LMA and Linklaters covering the RFR-related provisions in ISDA’s documentation, as well as how counterparties can hedge RFR-linked loans. The webinar recording is below. The slide presentation and other materials, is now available on the ISDA website.

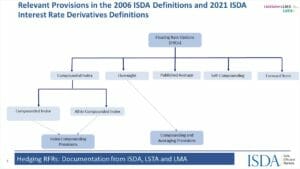

In anticipation of LIBOR’s upcoming cessation and the transition to risk-free rates (RFRs), ISDA has updated its standard definitions to include various rate options for different forms of RFRs, as well as provisions for compounding and averaging RFRs. While derivatives that trade in the overnight index swaps market are expected to continue to use the so-called “self-compounding” rate options, ISDA’s updates also allow for use of term RFRs and bespoke compounding to facilitate hedging of cash instruments that may use different forms of RFRs. In collaboration with LSTA and LMA, ISDA has also recently published several forms of confirmation for use in hedging loans that reference RFRs with various conventions. The forms of confirmation designed for use with the LSTA’s Daily Simple SOFR Concept Document (published in May 2021) is available here.