October 17, 2023 - At last week’s LSTA Annual Loan Conference, one intrepid panel set forth to try to quantify the risk and return of liability management transactions (LMTs). Long-time market observer Steve Miller of Fitch Solutions undertook the task of measuring the historical impact of LMTs on credit loss, and then applying those findings to future scenarios. Here are the slides that supported the panel. Below, we summarize the results published by Covenant Review.

There are a number of forms of LMTs, but we focused on the “Serta loophole,” which permits a majority group of lenders to i) provide new financing that takes priority over, or primes, the existing first lien financing and ii) elevates the pre-existing claims of the priming lenders above those of the primed (minority) lenders.

Let’s begin with stats and assumptions:

- Sixty-two percent of the loans in the CS Index have the Serta loophole.

- The average gap in the recovery of primed lenders and the weighted average recovery of primed and non-primed lenders has been 23 percentage points.

- Assuming that the future share of Serta loophole defaulted loans is the same as the Index (e.g., 62%), the incremental credit loss for a primed lender of a 1% increase in the default rate is 14 bps. (The conceptual math: 1% defaults*62% loans with Serta loophole*23 points additional LGD = 14 bps.)

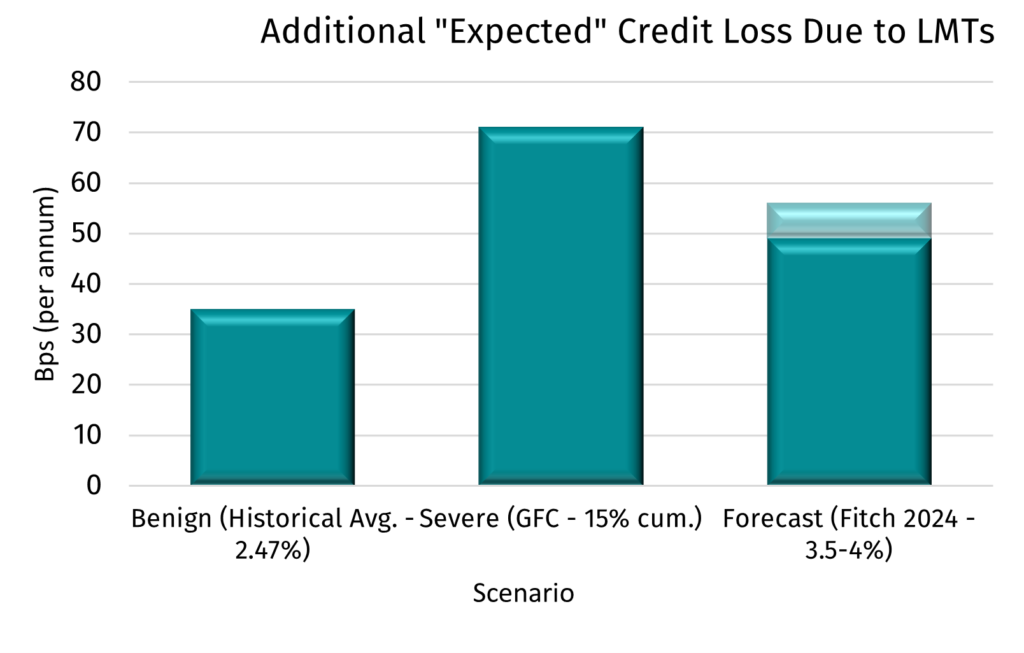

Next up: Scenario analysis (with the caveat that this is all theoretical and simply meant to illustrate an approach!).

- The benign scenario looks through history. The historical CS Index default rate is 2.47%. Multiply that by 14 bps additional LGD and the increase in annual expected credit loss is 35 bps.

- The severe scenario uses the Global Financial Crisis, where the cumulative three-year default rate was 15%; the same math leads to 71 bps of incremental credit loss per year.

- The forecasted scenario uses Fitch’s outlook of 3.5-4% default rates next year; in this case the incremental credit loss is 49-56 bps.

Now, of course the loan market has changed since the early-2000s when loan documents were covenanted up tight and “shenanigans” such as LMTs were unlikely to transpire. In addition to more secondary market liquidity (permitting loans of questionable character to be sold), loan spreads are significantly higher. According to Fitch, the nominal spread on the CS Index currently sits at 400 bps – well above the 315 bps average in 1999 and higher than the theoretical credit losses cited above.

Bottom line: Few lenders embrace LMTs and Fitch has discussed recent tactics to limit or de-risk LMT behavior. And while the future is unknowable, rather than simply demonizing LMTs – however demonic they might be – it may be worthwhile for loan practitioners to step back to assess how truly impactful they are to the loan market as a whole.